The Ceasefire Seesaw

April 13, 2026

Market Roundup & The Week in Review

The trading week of April 6th – 10th was a masterclass in headline-driven volatility, defined by a "Ceasefire Seesaw" that kept the bulls and bears in a constant tug-of-war. What began as a relief rally quickly hit a wall of reality as sticky inflation data and geopolitical skepticism took center stage.

Early-week optimism over a two-week ceasefire agreement and the reopening of the Strait of Hormuz sparked a massive risk-on surge. The S&P 500 jumped 3.56% and the Nasdaq 100 soared 4.45% for their second consecutive winning week, as the "war premium" temporarily evaporated.

The euphoria was dampened on Friday by a "hot" March CPI report. Headline inflation accelerated to 3.3% YoY, driven largely by the massive spike in gasoline prices (which have surpassed $4/gallon in many regions). This may have effectively reset expectations for the Fed, with the "higher-for-longer" narrative regaining its grip.

In a rare "barbell" performance, Crude Oil (WTI) plunged nearly 15% to close below the $100 threshold on the ceasefire news, while Big Tech provided a critical buffer for the indices. Investors were clearly favoring high-margin AI growth as a hedge against energy-driven margin compression in other sectors.

Strategy Corner

Based on this week's market movements, here are some trading ideas and option strategies for the readers' consideration. The positions can be scaled bigger (or smaller) to suit individual account size.

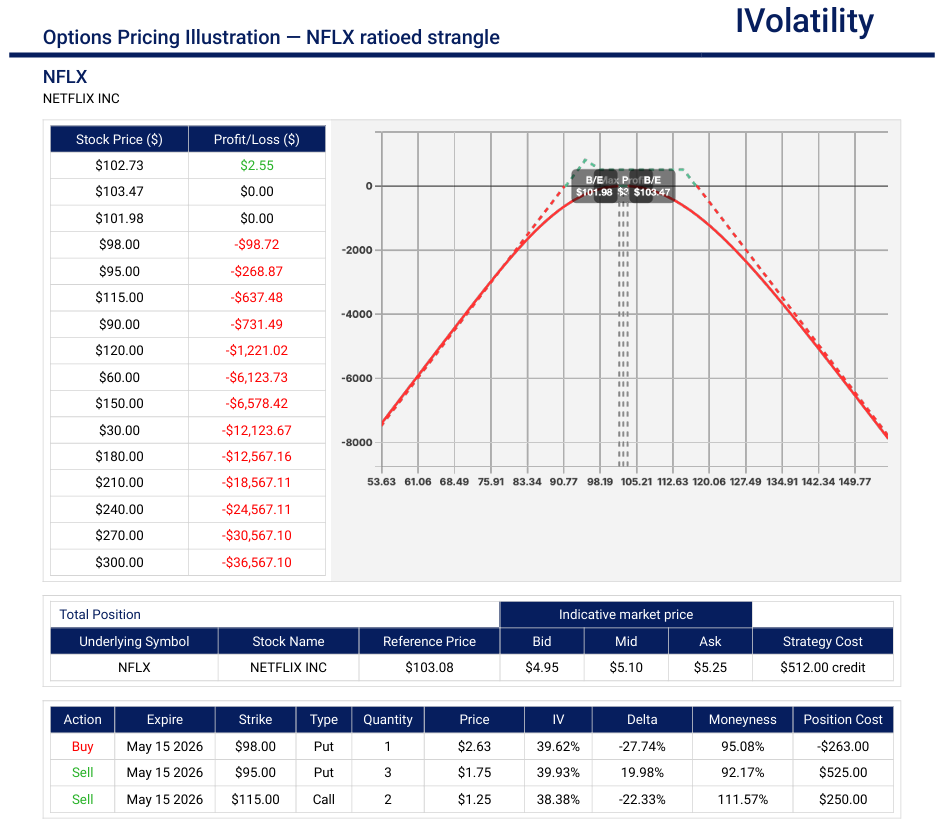

- NFLX (closed at 103.02 on Friday, Apr 10th)

With Netflix reporting earnings on April 16th, traders might look past this immediate binary event and position for May monthly expiration. While the "relief rally" in tech has provided a lift, the combination of sticky inflation data and a tightening consumer discretionary budget may suggest that NFLX could struggle to maintain its premium valuation if subscriber guidance shows any signs of cooling. - Strategy: Ratioed Strangle, leaning slightly bearish. to reflect a cautious, bearish-to-neutral bias.

- Setup: In the May15 expiration,

Buy one 98put / Sell three 95puts to create a 1 by 3 put ratio

Sell two 115calls to now create the Ratioed Strangle - Credit received: $500

- Probability of profit: around 70%

- Breakevens: around: 91 and 118

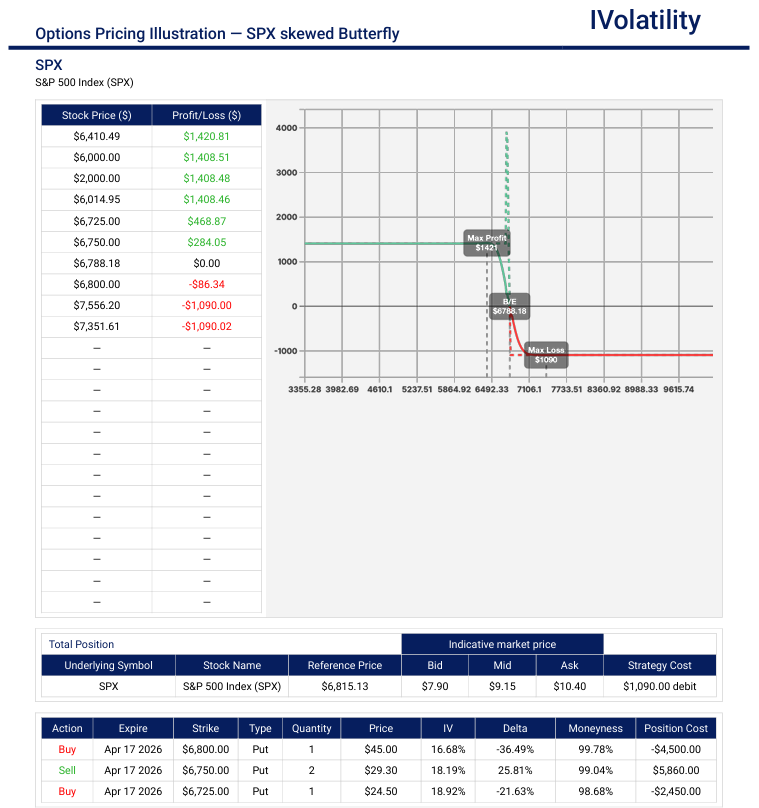

- SPX (closed at 6816.89 on Friday, Apr 10th)

With the failure of the ceasefire and the "hot" CPI data still being digested, the market is facing a significant momentum stall. While a violent "trapdoor" sell-off has not occurred yet, the technicals may suggest a heavy, grinding move lower as the "war premium" is re-priced and Fed expectations shift. - Strategy: Skewed Put Butterfly

- Set up: On Monday, April 13th, open the following position for Apr 17th expiration

Buy one OTM put / Sell two OTM puts 50pts away / Buy one OTM put 75pts away

The trader will pay a debit for this skewed butterfly with the near wing $50 wide and the far wing $25 wide - Risk: Debit paid for the purchase; no risk to the downside

- Max Potential Profit: Occurs with expiration around the short puts and equals the width of the near wing LESS the debit paid for the purchase.

Movement of the Major Market Indices:

It was a volatile week as the market grappled with the fifth week of the conflict around the Persian Gulf. After a sharp initial sell-off that pushed major indices toward correction territory, a late-week "snap back" helped recover some ground.

| INDEX | UP | DOWN |

| SPY | 3.56% | |

| QQQ | 4.68% | |

| IWM | 3.97% | |

| DIA | 3.04% | |

| GLD | 2.80% | |

| BTC/USD | 5.40% | |

| 10-year yield | 1.50% | |

| Crude Oil | -4.20% | |

| VIX | -19.54% |

Movement of the Major Market Sectors:

The week was defined by a powerful risk-on rotation as growth-oriented sectors capitalized on a significant drop in volatility. XLK and XLY led the charge, rebounding sharply as the market moved past the recent geopolitical "correction scare." Conversely, XLE was the lone outlier in the red, seeing profit-taking as oil prices stabilized and the immediate rush for inflation hedges cooled. Overall, the breadth was strong, with defensive sectors like XLP and XLU trailing but remaining positive, signaling a healthy, broad-based recovery across the board.

| SECTOR | UP | DOWN |

| TECH (XLK) | 5.12% | |

| FINANCIALS (XL) | 2.85% | |

| INDUSTRIALS (XLI) | 3.10% | |

| ENERGY XLE | -1.45% | |

| HEALTHCARE (XLV) | 2.15% | |

| UTILITIES (XLU) | 1.05% | |

| MATERIALS (XLB) | 2.90% | |

| REAL ESTATE (XLRE) | 3.40% | |

| CONSUMER STAPLES (XLP) | 1.20% | |

| CONSUMER DISCRETIONARY (XLY) | 4.75% |

Notable gainers for the week of Apr 6th–Apr 10th:

The week was dominated by a powerful "relief rally" following the ceasefire news, which sparked a massive short-covering surge in high-growth tech and consumer-facing names that had been beaten down during the March volatility.

The gainers were heavily concentrated in Technology (XLK) and Consumer Discretionary (XLY). The common thread was a pivot away from "inflation hedges" back into "innovation and growth." Names with high fuel-cost sensitivity, like the airlines, saw some of their best weekly performances of the year as the energy-driven pressure on margins suddenly evaporated.

- NVDA popped over 11% led by the "risk-on" charge as semi-conductors rebounded; investors rushed back into AI growth names as the geopolitical discount faded.

- TSLA jumped over 9% appearing to benefit significantly from the drop in crude oil prices and the reopening of global trade routes, easing supply chain and logistical fears.

- UAL surged nearly 13% as the -15% drop in WTI Crude directly lowered projected fuel costs, combined with an associated surge in travel bookings post-ceasefire.

- AMD rose nearly 9%, probably in strong sympathy with NVDA, boosted by reports of stabilized chip demand in the EMEA region.

- DKNG popped 10% and was a standout in the Consumer Discretionary sector as retail sentiment shifted back toward speculative growth and leisure spending.

Notable losers for the week of Apr 6th–Apr 10th:

While the broader market celebrated the ceasefire, the "flight-to-safety" and "inflation-hedge" trades were aggressively unwound. Stocks that had benefited from the geopolitical tension and high energy prices saw significant profit-taking.

The "losers" list this week is almost a perfect mirror of the winners from late March. The Energy (XLE) and Materials (XLB) sectors felt the most pain as the "ceasefire euphoria" drove a total reversal of the inflation trade. Defensive "bond-proxy" stocks in the Utilities (XLU) and Staples (XLP) sectors also lagged significantly as capital sought higher returns in the rebounding growth sectors.

- RBRK shed nearly 15% as the market favored “Big AI” (NVDA, AVGO).

- SAIL dumped over 19% as investors rotated away from mid-tier security plays into the broader index rally.

Review selected market indices below:

Daily Notable Market Action

This week marked a dramatic shift in market sentiment, transitioning from geopolitical anxiety to a powerful "relief rally" as diplomatic breakthroughs dominated the headlines.

Monday's Markets and News:

The week began with cautious optimism. Markets drifted higher as investors monitored diplomatic signals regarding the Strait of Hormuz. While the S&P 500 managed a +0.4% gain, trading volumes remained light as the "wait-and-see" approach prevailed ahead of the mid-week deadlines.

Tuesday's Markets and News:

Traders saw a tug-of-war session in the markets. Early morning fears of escalation sent oil prices higher, briefly dragging on the indices. However, a late-afternoon surge in Nvidia (+2.2%) and other semi-conductors helped the Nasdaq decouple from the broader market's choppiness, closing in the green despite a lackluster performance from the Dow.

Wednesday's Markets and News:

This was the definitive "turn" for the week. Global markets erupted after a two-week ceasefire agreement was officially announced, alongside the reopening of the Strait of Hormuz. The S&P 500 jumped +2.5% and the Dow surged +2.85%in its best single-day performance of the year, while WTI Crude plummeted 15% back toward $96/barrel.

Thursday's Markets and News:

Thursday saw a natural cooling-off period. The "ceasefire euphoria" faded into a soberer assessment of the truce's longevity. Equities moved sideways for most of the day as investors digested the rapid price changes in the energy and bond markets, leading to a mixed close.

Friday's Markets and News:

The week concluded with a focus on domestic data. The March CPI report showed a 3.3% year-over-year increase—high, but lower than the "energy-shock" extremes many had feared. This allowed the Nasdaq to squeeze out a final +0.4% gain as investors settled into positions ahead of high-level US-Iran talks scheduled for the weekend.

Notable Earnings (Apr 13th–Apr 17th)

As the Q1 2026 earnings season kicks off, the market's focus might shift from geopolitical headlines to corporate fundamentals. The coming week is heavily weighted toward the financial sector, providing a critical health check on the banking industry following the recent energy price spikes and interest rate volatility. These reports will set the tone for whether the early April relief rally has the fundamental legs to continue.

The actual earnings date may vary, so traders should confirm with their brokers. If a trader wishes to open a position to participate in earnings announcements, it is important to check whether the earnings are released BEFORE the markets open or AFTER the markets close on the date of earnings.

Monday, Apr 13th: GS / FAST

Tuesday, Apr 14th: JPM / JNJ / WFC / C / BLK / KMX

Wednesday, Apr 15th: BAC / MS / PGR / PNC

Thursday, Apr 16th: NFLX / PEP / SCHW / BK / USB / TSM / FCX / TRV

Friday, Apr 17th: AXP / PG / SLB / ALLY / FITB

Economic Calendar (April 13th – April 17th:)

With the ceasefire in potential jeopardy, the market is once again navigating a "double-threat" environment. Traders are forced to balance a high-stakes geopolitical risk premium with a heavy slate of domestic data. The volatility in energy prices remains the primary wildcard, meaning the week’s inflation and consumer spending reports will be viewed through the lens of a "war-time economy." Traders might experience higher-than-normal sensitivity to any data that suggests the Fed's hands are tied by persistent, energy-driven price pressures.

The daily schedule of notable economic data releases is:

Monday (4/13): Consumer Inflation Expectations

This NY Fed survey is critical. If consumers expect inflation to stay high due to the renewed conflict, it risks a "wage-price spiral" that would force the Fed to stay aggressive despite slowing growth.

Tuesday (4/14): NFIB Small Business Optimism Index

This is a measure of the "backbone" of the economy. Traders will look to see how small businesses are coping with renewed supply chain uncertainty and whether higher costs will continue to be passed on to consumers.

Wednesday (4/15): Retail Sales (March)

Given the collapse of the truce, investors would like to determine if the American consumer is starting to pull back on discretionary spending (XLY) as gas prices climb again.

Thursday (4/16): Initial Jobless Claims & Philly Fed Manufacturing Index

This provides a dual-view of the economy. Jobless claims monitor labor market cracks, while the Philly Fed serves as a leading indicator for industrial health (XLI) amid rising input costs.

Friday (4/17): Consumer Sentiment (Preliminary)

This index tracks the psychological impact of the news cycle. A sharp drop in sentiment would signal that the renewed geopolitical tension is directly hitting consumer confidence, likely leading to a defensive rotation into XLP and XLU.

Something to think about...

California's building regulations are some of the strictest in the world. So when the state gives a "thumbs-up" to a new kind of housing model, it has the potential to send ripples through the $10 Trillion global market.

A company called Geoship is creating that ripple. It has not only received California's Factory-Built Housing (FBH) certification, but 3,200+ homebuyers have signaled demand for Geoship's bioceramic dome-homes.

Designed by a team of engineers from Tesla, Toyota, and Apple, these domes can be installed 9x faster than traditional construction, with 50% lower construction costs at scale. Designed to last 500 years, they're resilient to wildfires, hurricanes, and earthquakes.

Geoship is treating a home like a manufactured product rather than a construction project. Founded on the principles of the legendary polymath Buckminster Fuller, the company has combined nature's most efficient shape—the geodesic dome—with a breakthrough in material science called bioceramics. Most modern homes are built with wood, concrete, and toxic adhesives that are vulnerable to mold, fire, and termites. Bioceramics, which have a molecular structure similar to human bone or sea shells, are essentially "ceramic rocks" that don't burn, rot, or rust.

Beyond the individual house, Geoship is focused on regenerative communities. They operate as a Social Purpose Corporation, meaning they are legally bound to prioritize their mission over pure profit. Their vision includes "Village Builder" platforms where people can use AI and blockchain to co-finance and design decentralized, off-grid neighborhoods. By focusing on non-toxic materials and "sacred geometry," they aim to create living spaces that actually improve human health (better air quality, no off-gassing) rather than just providing a roof over one's head.

Because of the geodesic shape, these domes are naturally aerodynamic and structurally superior to traditional "box" houses. They are engineered to withstand Category 5 hurricanes, massive snow loads, and high-magnitude earthquakes. In an era where insurance companies are pulling out of high-risk areas like Florida and California due to climate volatility, a fireproof and flood-resilient home may no longer be just a "green" choice—it could be a financial necessity. Geoship's goal is to make these homes 30% to 60% cheaper than conventional builds through modular, factory-based manufacturing. For us as investors and observers of the macro-economy, this represents a potential disruption of the $10 trillion global housing market. It moves the needle away from "disposable architecture" toward permanent, non-toxic, regenerative communities.

Geoship already has $500 Million in deposit-backed reservations and the delivery of their first homes is scheduled for late 2026.

Questions / Comments

We're here to serve IVolatility users and we welcome your questions or feedback about the option strategies discussed in this newsletter. If there is something you would like us to address, we're always open to your suggestions. Use support@ivolatility.com.

Previous issues are located under the News tab on our website.